how do we know the frivolous penalty is bogus?

proof the irs is committing fraud against we the people

“Persons dealing with the government are charged with knowing government statutes and regulations, and they assume the risk that government agents may exceed their authority and provide misinformation.”

Lavin v. Marsh, 644 F.2d 1378 (9th CA, 1981) {emphasis added}

what if you had incontrovertible proof the irs is committing fraud? would you stand against them on principle, even though they appear to have the upper hand? or would you just let it slide or pretend not to notice? [or for believers - wwjd?]

let’s take a closer look at this frivolous return penalty so you can decide for yourself whether these agents have exceeded their authority.

after our refusal to incorporate the incorrect forms w-2 into our returns at the behest of the irs per letter 12c, the irs then sent letter 3176c (see the bottom of part one), for both 2019 and 2020, which states:

“You filed a purported tax return for the tax periods above that claimed one or more frivolous positions or reflected a desire to delay or impede administration of the tax laws. If you don't immediately correct your return, we'll assess a $5,000 penalty against you.” {emphasis added}

the two bolded statements above are important because they are a specific reference to the code, further clarified in the next paragraph:

“Based on Internal Revenue Code Section 6702, Frivolous Tax Submissions, we determined the information you filed as a purported tax return … is frivolous and there is no basis in the law for your position.” {emphasis added}

in our response (see the top of part two), we provided an affidavit where we swore under penalty of perjury that we did not claim any position and had no desire to delay or impede administration of the tax laws.

both the subsequent letter 3175c and the notices cp15 that assess the penalty state the provisions in the code:

§6702. Frivolous tax submissions

(a) Civil penalty for frivolous tax returns

A person shall pay a penalty of $5,000 if-

(1) such person files what purports to be a return of a tax imposed by this title but which-

(A) does not contain information on which the substantial correctness of the self-assessment may be judged, or

(B) contains information that on its face indicates that the self-assessment is substantially incorrect, and

(2) the conduct referred to in paragraph (1)-

(A) is based on a position which the Secretary has identified as frivolous under subsection (c), or

(B) reflects a desire to delay or impede the administration of Federal tax laws. {emphasis added}

the highlighted provisions in (2)(A) and (2)(B) align with the statements in letter 3176c bolded above.

the structure of code section 6702(a) is:

IF

{(1)(A) OR (1)(B)}

AND

{(2)(A) OR (2)(B)}

THEN

“PERSON” SHALL PAY PENALTY OF $5000 {“person” is in quotes because it is a term defined in the code}

but what’s missing from both letters and the notice is which of (2)(A) or (2)(B) applies to my return. also missing is which of (1)(A) or (1)(B) applies. because there is an AND between them, for the penalty to apply then both (1) AND (2) need to be satisfied.

our sworn affidavit (shown in part two) addresses all four of these:

item #1 states our return in fact does contain information on which the substantial correctness of the self-assessment may be judged, so (1)(A) does not apply

item #2 states our return in fact does not contain information that on its face indicates that the self-assessment is substantially incorrect, so (1)(B) does not apply

we could stop there because if neither (1)(A) or (1)(B) applies, then there can be no penalty applied. but we continued:

item #3 states our return in fact is not based on any position which the Secretary has identified as frivolous, so (2)(A) does not apply

item #4 states our return in fact does not reflect a desire to delay or impede the administration of federal tax laws, so (2)(B) does not apply

again, we could stop there because we’ve shown none of the provision of 6702(a) apply, but we didn’t stop, we also swore in item #5 that the “person” who shall pay the penalty doesn’t apply to us either:

§6671. Rules for application of assessable penalties

(a) Penalty assessed as tax

The penalties and liabilities provided by this subchapter shall be paid upon notice and demand by the Secretary, and shall be assessed and collected in the same manner as taxes. Except as otherwise provided, any reference in this title to "tax" imposed by this title shall be deemed also to refer to the penalties and liabilities provided by this subchapter.

(b) Person defined

The term "person", as used in this subchapter, includes an officer or employee of a corporation, or a member or employee of a partnership, who as such officer, employee, or member is under a duty to perform the act in respect of which the violation occurs. {emphasis added}

what could be the reason the irs has completely ignored our sworn testimony? they have made no effort to show how any of this applies to us and we have made every effort to show that it does not.

but it gets worse, because if we take a closer look at (2)(A) above it references, “a position which the Secretary has identified as frivolous under subsection (c)”

(c) Listing of frivolous positions

The Secretary shall prescribe (and periodically revise) a list of positions which the Secretary has identified as being frivolous for purposes of this subsection. The Secretary shall not include in such list any position that the Secretary determines meets the requirement of section 6662(d)(2)(B)(ii)(II). {emphasis added}

helpfully, the third paragraph of letter 3176c tells us where to look for that specific list:

“Notice 2010-33 provides detailed information on positions identified as frivolous under Section 6702.”

you can read the notice yourself here. there are 46 numbered items. there’s also this sentence at the bottom of the purpose section, which again, doesn’t apply to our return:

“The penalty will be imposed only when the frivolous position or desire to delay or impede the administration of Federal tax laws appears on the face of the return, purported return, or specified submission, including any attachments to the return or submission.” {emphasis added}

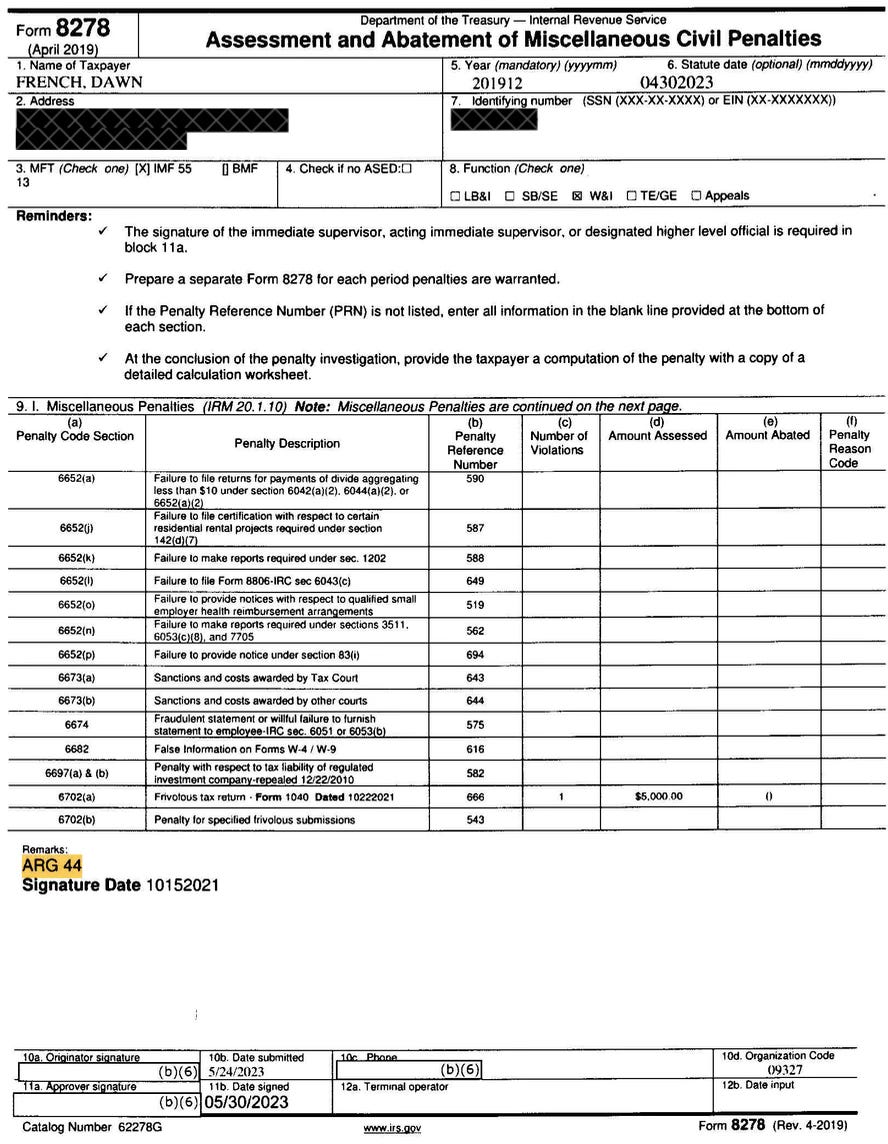

now let’s take a look at form 8278, which i received through my foia request:

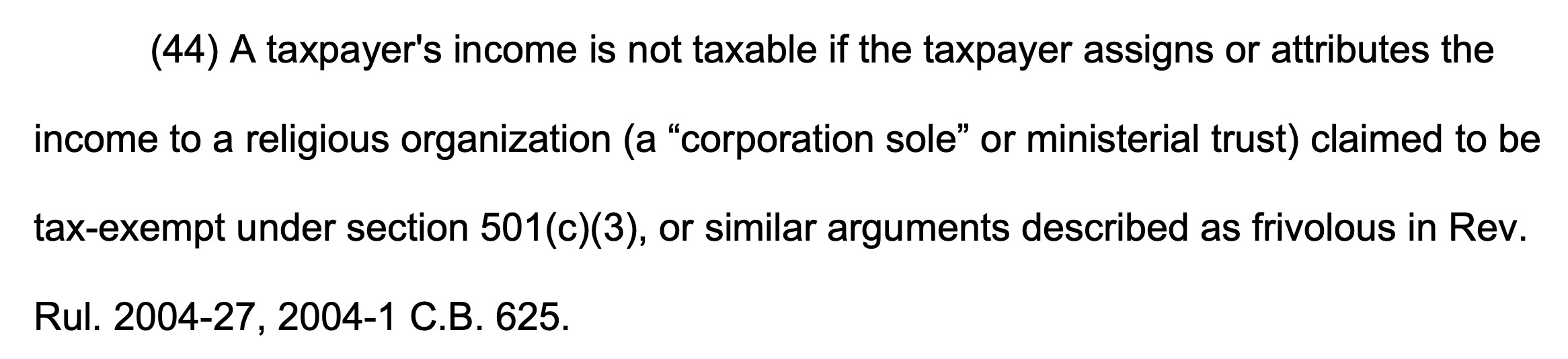

notice the highlighted ARG 44 under remarks. now let’s look at numbered item 44 on notice 2010-33:

huh. that definitely doesn’t apply to our return. so what’s going on here?

here’s where the blatant fraud comes in. let’s go to the irm - the internal revenue manual, part 25, chapter 25, section 10 frivolous return program, exhibit 25.25.10-1 frivolous arguments:

Frivolous arguments are currently described in Notice 2010-33, available at https://www.irs.gov/irb/2010-17_IRB#NOT-2010-33 (or its successor notice), the Truth About Frivolous Arguments, and a number of revenue rulings. Please refer to these publications for the most current listing of frivolous arguments. Recognized frivolous arguments include but are not limited to… {emphasis added}

the 44th item in this lettered list (letters instead of numbers), is item #ar:

ar. Zero Wages on a Substitute Form: Taxpayer generally attaches either a substitute Form W-2, Form 1099, or Form 4852 that shows "$0" wages or no wage information. A statement may be included indicating the taxpayer is rebutting information submitted to the IRS by the payer. Entries are usually for Federal Income Tax Withheld, Social Security Tax Withheld, and/or Medicare Tax Withheld. An explanation on the Form 4852 may cite "statutory language behind IRC 3401 and IRC 3121" , or may include some reference to the company refusing to issue a corrected Form W-2 for fear of IRS retaliation.

that just describes the procedure that every individual should follow if their w-2 were incorrect. an actual position is not WHAT you do, or HOW you do it, it is WHY you do it.

item #ar it IS NOT a “position” and DOES NOT appear anywhere on notice 2010-33.

someone deliberately included that item #ar in the internal revenue manual knowing it is NOT a position which the Secretary has identified as being frivolous, in order to commit extortion under color of law. that’s proof the irs is committing fraud.

if not fraud, someone please give me a reason why that item #ar is listed under recognized frivolous arguments in the irm but not in notice 2010-33 and

does our licensed cpa have a response to what is clearly fraudulent behavior by the irs?

the above is just one example among many. i will continue to share more examples in future posts.

how about you, dear reader? do you believe the irs is being deceitful or honest?

"Cowardice asks the question - is it safe? Expediency asks the question - is it politic? Vanity asks the question - is it popular?

But conscience asks the question - is it right? And there comes a time when one must take a position that is neither safe, nor politic, nor popular; but one must take it because it is right."

~Dr. Martin Luther King, Jr.

life doesn’t come with any guarantees. we may lose this fight*, but does that mean we shouldn’t stand up to tyranny?

[*edit 11/13/23 -

to be clear, we’re not at all assuming we’ll lose this battle. we are actually pretty confident if they were really following the law, they wouldn’t need all the lies, obfuscations and fear porn to get us to comply. the comment was just meant to declare our resolve to stand up on principle even if the odds were firmly stacked against us.

as a purple belt in brazilian jiu jitsu, i just love to spar. and with that experience comes the ability to sense when you’re opponent if faking the funk. and i’m pretty sure anyone else following this saga closely can smell just how funky the irs is behaving here. and the comments from the trollery just make the smell even worse.]

anyone else get the sense the troll is desperate for you to not look behind the curtain?

“life doesn’t come with any guarantees. we may lose this fight, but does that mean we shouldn’t stand up to tyranny?”

Look, if you were there first person to come up with this harebrained scheme, one might think, “hey why not try it?”

But, you’re not the first. You’re not even the hundredth. Hundreds of people have tried this. The answers to all your questions are in the Tax Court and district court records. It’s been addressed. Thousands of times. You just don’t have a clue about tax law and so you think you’re onto something clever because of something you read on the internet, but you’re not. All this is going to be for you is a very, very expensive learning experience. I’ve had a few of those, one was probably as expensive as this is going to be for you- and it made me a better person. Hmm, there wasn’t a chance of jail though, so YMMV.