excerpts from my unsworn declaration - final

tales from tax court - episode six

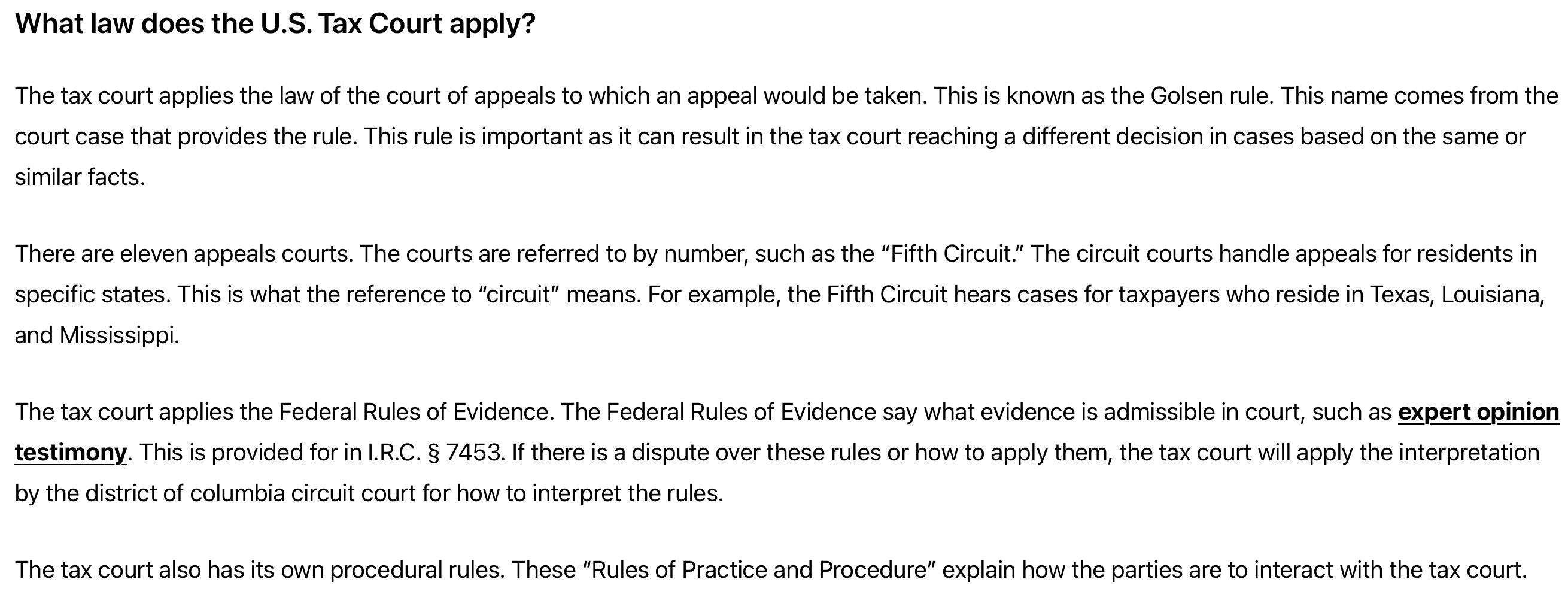

per this “definitive guide to tax court”

the tax court judge should apply the law of the fifth circuit, because we reside in texas.

however, there have been a few concerning rulings by the fifth circuit court of appeals with regard to the income tax, as we discovered when researching information on the irs’ website in this article:

did we fall for an internet scam?

yes, we did fall for an internet scam. just not the one you’re thinking.

i wanted to make sure to let the judge and the irs’ attorneys know, and the fifth circuit in case an appeal would be necessary, that the previous fifth circuit rulings were in error and should not be the “law” applied to our case.

See Young v. Comm’r, 551 F. App’x 229 (5th Cir. 2014)

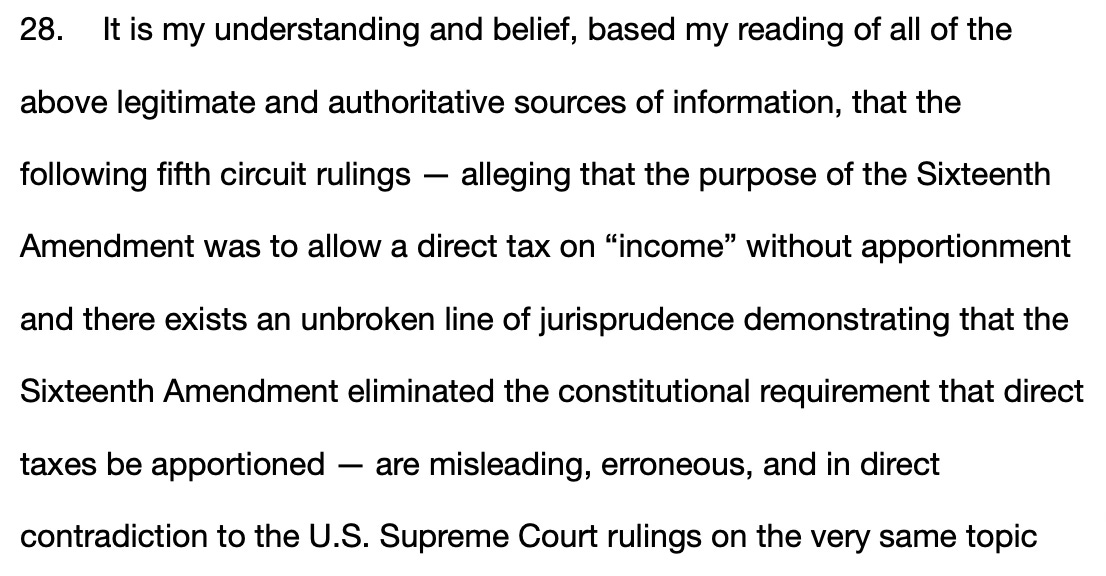

In regards to the income tax, suffice it to say, "[a]t this late date, it seems incredible that we would again be required to hold that the Constitution, as amended, empowers the Congress to levy an income tax against any source of income [Congress already had the power to levy an income tax before the 16th amendment], without the need to apportion the tax equally among the states [indirect taxes do not need to be apportioned], or to classify it as an excise tax applicable to specific categories of activities [this directly contradicts the U.S. Supreme Court that explicitly states that income taxes are indeed classed “under the head of excises, duties and imposts,” which are indirect taxes that “are the familiar federal taxes imposed on activities or transactions,” per the Moore excerpts above]." Parker v. Commissioner, 724 F.2d 469, 471-72 (5th Cir. 1984). We see no need to further defend a tax system that has been uniformly upheld.

See Parker v. C.I.R., 724 F.2d 469 (5th Cir. 1984)

Parker maintains that "the IRS and the government in general, including the judiciary, mistakenly interpret the sixteenth amendment as allowing a direct tax on property (wages, salaries, commissions, etc.) without apportionment." As we observed in Lonsdale v. CIR, 661 F.2d 71 (5th Cir. 1981), the sixteenth amendment was enacted for the express purpose of providing for a direct income tax [this directly contradicts the U.S. Supreme Court that explicitly states that the express purpose of the 16th amendment was to prevent using the source of “income” to remove income taxes from the indirect class to which they by nature belong and place them in the direct class, per the Brushaber excerpts above].

and

The thirty words of this amendment are explicit: "The Congress shall have power to lay and collect taxes on income, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration." The Supreme Court promptly determined in Brushaber v. Union Pacific Ry. Co., 240 U.S. 1, 36 S.Ct. 236, 60 L.Ed. 493 (1916), that the sixteenth amendment provided the needed constitutional basis for the imposition of a direct non-apportioned income tax [the U.S. Supreme Court promptly determined in Brushaber that the obviously intended purpose of the 16th amendment was to prohibit the placing of an inherently excise-like income tax into the direct tax class based on the source of the “income” and that the appellant’s erroneous “contention that the Amendment treats a tax on income as a direct tax although it is relieved from apportionment” is “wholly without foundation”].

and

The sixteenth amendment merely eliminates the requirement that the direct income tax be apportioned among the states [this is misleading because income taxes are in the indirect class, which are not required to be apportioned, per the above]. The immediate recognition of the validity of the sixteenth amendment continues in an unbroken line. See e.g. United States v. McCarty, 665 F.2d 596 (5 Cir. 1982); Lonsdale v. CIR.

See United States v. McCarty, 665 F.2d 596 (5th Cir. 1982)

In his appeal from the conviction itself, the defendant complains of inadequate instructions and also that he was not subject to any federal income tax since the Sixteenth Amendment did not really change the former constitutional requirement that direct taxation be apportioned according to population. This latter argument is made in the face of the express language of the Amendment, its undoubted express intention, and an unbroken line of jurisprudence to the contrary [the “unbroken line of jurisprudence” is NOT to the contrary as the U.S. Supreme Court repeatedly confirms that the 16th amendment did not change the constitutional requirement that direct taxes be apportioned]. See, e. g., Lonsdale v. C.I.R., 661 F.2d 71, 72 (5th Cir. 1981).

See Lonsdale v. C.I.R., 661 F.2d 71 (5th Cir. 1981)

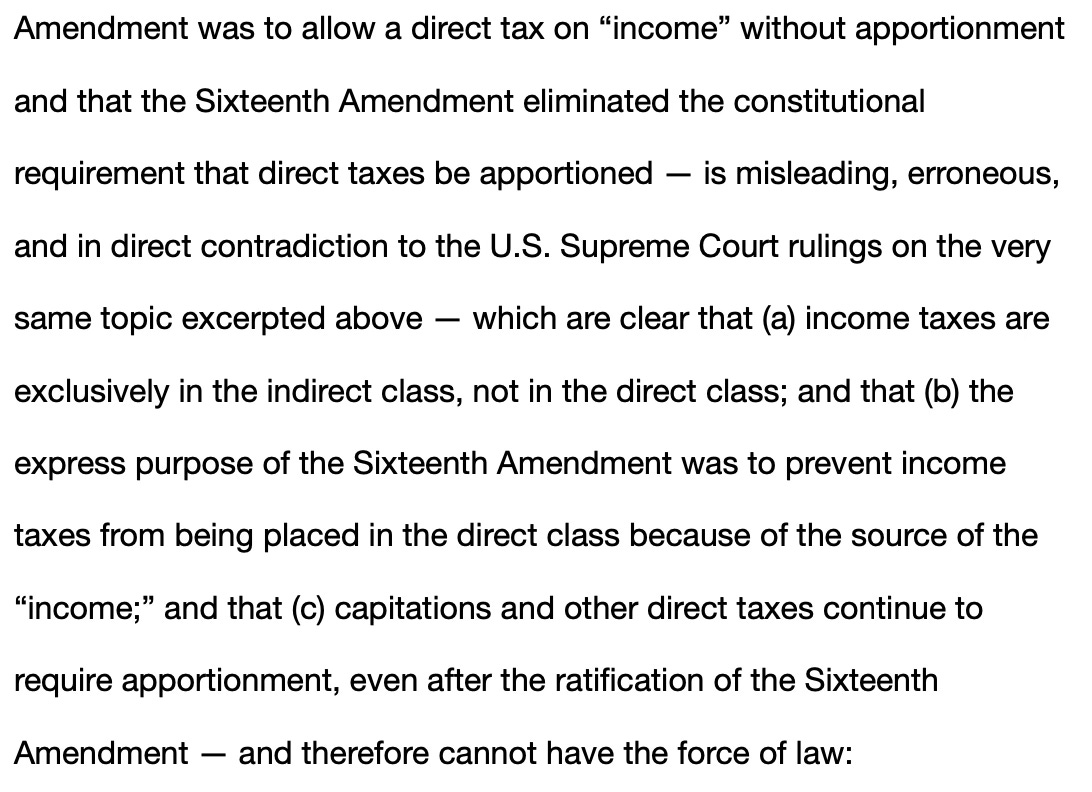

Appellants next seem to argue, in reliance on Pollock v. Farmers Loan Trust Co., 157 U.S. 429, 15 S.Ct. 673, 39 L.Ed. 759 (1895), and other authority, that, so understood, the income tax is a direct one that must be apportioned among the several states. U.S. Const. art. I, sec. 2. This requirement was eliminated by the sixteenth amendment [there is no citation provided and this directly contradicts the U.S. Supreme Court that repeatedly confirms that income taxes are in the indirect class and therefore not required to be apportioned, and that the 16th amendment did not eliminate the constitutional requirement that direct taxes be apportioned].

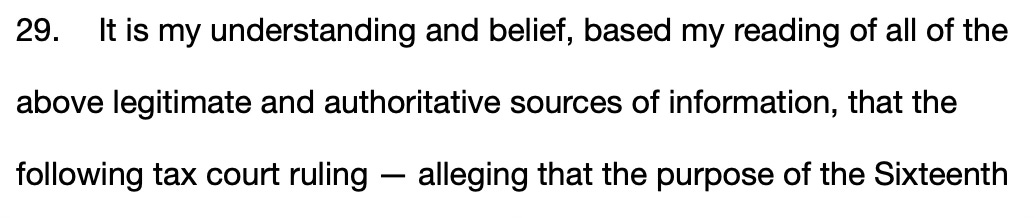

the blatant errors in one of the tax court cases that was used as a citation in the irs’ motion for summary judgment against us also needed to be addressed; and this case had also made an appearance in the comments of one of my other articles here.

See Waltner v. Comm’r, T.C. Memo. 2014-35 (U.S.T.C. Feb. 27, 2014)

Starting with the premise that taxes are either direct or indirect, Cracking the Code lays the foundation for the remainder of the book on two fallacies. The first is that "federal direct taxes which affect citizens of the several states must be apportioned [this statement is not a fallacy per the U.S. Supreme Court that confirms direct taxes are and have always been required to be apportioned].” The Constitution at one time required this apportionment [per the Moore excerpts above, the Constitution continues to require apportionment for direct taxes]; however, with the adoption of the 16th Amendment in 1913, this rule no longer applies to income taxes [this is misleading because income taxes are in the indirect class and therefore the apportionment rule does not apply, and the 16th amendment did not change that, only that the source of “income” cannot be used to place income taxes in the direct class]. It is unclear whether the author accepts this fundamental point [it is unclear whether this judge understands this or is being deliberately vague and misleading].

and

A similar problem adheres to the author's discussion of Pollock v. Farmers' Loan & Trust Co., 158 U.S. 601 (1895). The case addressed the question of direct versus indirect taxes and the (then-existing) requirement that all direct taxes be apportioned [Moore confirms the requirement that all direct taxes be apportioned still exists, so by definition cannot accurately be described as “then-existing”]. Again, the apportionment issue was resolved by the 16th Amendment, which was proposed and ratified after Pollock [the U.S. Supreme Court confirms that the 16th amendment did not resolve any “apportionment issue,” it resolved the source issue, and in fact stated that the obviously intended purpose of the 16th amendment was to prohibit the placing of an income tax into the direct tax class based on the source of the “income”, and that indirect taxes are not required to be apportioned]. The author's failure to recognize this simple point renders the rest of his discussion meaningless [this judge's failure to recognize his own obvious errors renders the rest of his discussion on the topic suspect].

these examples of tax court and fifth circuit court rulings should concern you.

if you are not vigilant, these well-paid judges and attorneys will attempt to bamboozle you with bullshit.

pay attention to how their language is deliberately misleading. this is just a sample.

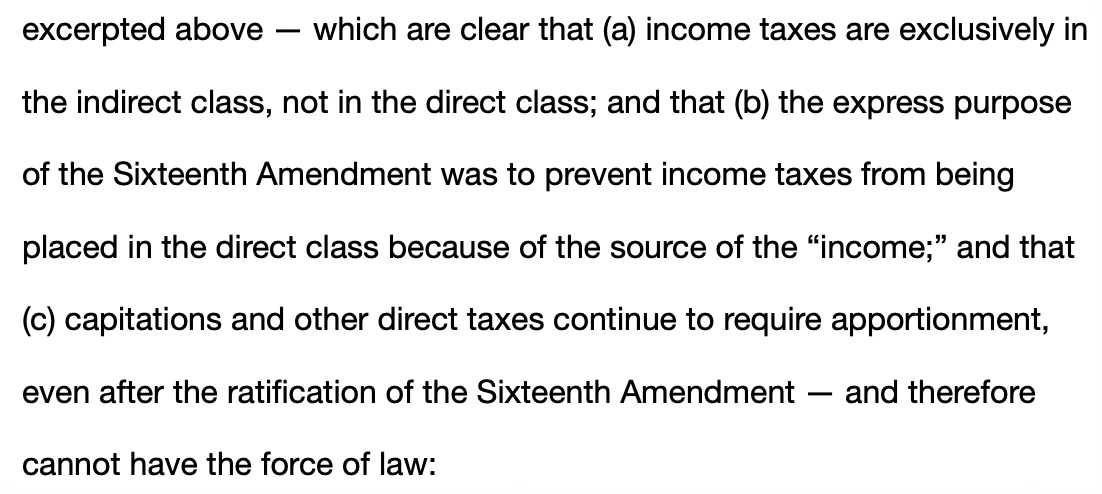

coming up next is a series of posts documenting my interactions with a senior lecturer at one of the law schools here in texas. i will point out specifically every time this “expert” contradicts himself and provides mis/dis/mal-information.

i’ll break it down for you and show you exactly how the “experts” lie so you will be able to see it coming.

thanks for reading and sharing!